New research shows that 52 per cent of decision makers in financial services have implemented blockchain because of its speed and cost benefits. Nearly a third are planning to invest in blockchain in the future and 14 per cent admit they should be considering investment despite having no plans for it at the moment.

This according to recruitment specialist, Robert Half Financial Services, which also projects a future skills gap for the sector.

Blockchain, as a ledger system, automates and records transactions which can be accessed by all the parties involved in the payment or lending processes. Eliminating the need for saving copies of invoices, bills and financial statements.

As the appetite for blockchain grows, so is the demand for people with the right skills to maximise the technology. Organisations are seeking out financial services professionals with a deep understanding of the principles surrounding blockchain systems listing technology trading (51 per cent ) and programming (47 per cent) as the skills most in demand.

“Automation is changing the face of business, and particularly so within the skills and roles within the financial services industry,” explained Matt Weston, director at Robert Half Financial Services. “With financial crime and compliance high on the priority lists for many senior leaders in financial services, attracting skilled specialists to support the implantation is key. To keep up with the rapidly changing skill and role development, companies who adopt a flexible recruitment strategy will be best placed to adapt their resource requirements during this change.”

https://growthbusiness.co.uk/hindsight-2020-top-tech-wins-backed-recent-history-2551527/

Overall, 85 per cent of financial services executives believe blockchain will have made a genuine impact on the financial services industry by 2022. Those that have implemented blockchain report already experiencing benefits including empowered users, increased transparency and faster transactions. While respondents that have not yet experimented with blockchain see the opportunity that it offers to achieve faster transactions, lower transaction costs and user empowerment.

Blockchain is the public ledger technology underpinning Bitcoin but the technology has also launched other innovations, and is increasingly gaining prominence in sectors beyond financial services. Its appeal ranges from its mysterious beginnings to the shroud of controversy that still lingers over the terminology.

No one can definitively tell who is behind blockchain technology. The first person to conceptualise the technology went by the alias Satoshi Nakamato. But who is this Satoshi Nakamoto? It is it an individual or a group of innovators? Nakamato is credited for creating Bitcoin (cryptocurrency), of which blockchain is fundamental.

The controversy surrounding blockchain is largely because it undermines and questions all of the existing standards and protocols in place for recording transactions. For banks, change has been the only constant since the 2007 crash, so adopting and keeping up with blockchain has been particularly challenging. Within financial services, traditional banks have not been first-movers and struggle to keep up with competitors.

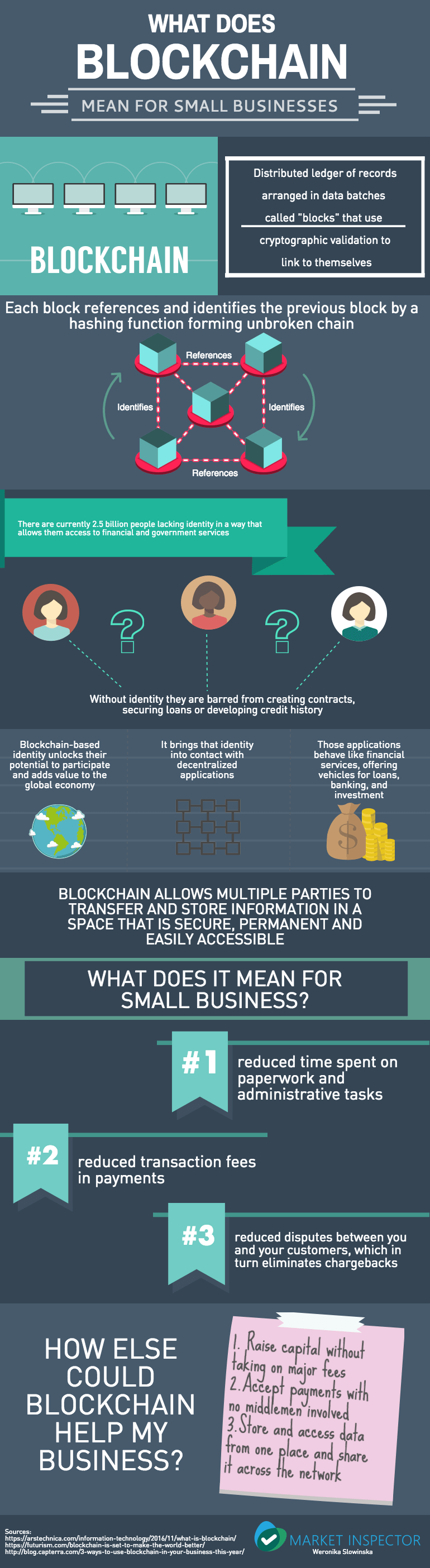

Complicated: Starting to learn about blockchain is like trying to solve sudoku for the first time. At the beginning, it might appear complicated but, eventually, it makes sense. Blockchain is a decentralised ledger in which data batches (blocks) use cryptographic validation to link themselves together. It is based on a mathematical equation which actually acts as an authority. It exists on multiple computers at the same time in such a way that anybody with an interest can maintain a copy of it, and can only be changed when there is a consensus among the group. Moreover, old transactions in the ledger are preserved forever and new transactions are added to it irreversibly. This system has the potential to make the lives of individuals, as well as business owners, much easier.

This infographic from Market Inspector dissects blockchain and its applications for small businesses.

Related Stories

Taking payments

Cheapest card payment providers

Here are the cheapest card payment machines for growing businesses, including SumUp, Revolut, Square, Zettle.